This website uses cookies to improve your browsing experience.

GDPRBetter Decisions.

Smarter Insurance.

Real Impact.

K2G enables insurance leaders to make high-stakes decisions with confidence — by combining AI, data, and human judgment.

THE CHALLENGE

Insurance Leaders are not lacking data.

They are lacking clarity.

The insurance industry is under pressure to adapt—faster, smarter, and more precisely than ever before. Yet many organizations struggle to translate AI, data, and strategy into better decisions.

OUR APPROACH

K2G Improves how insurance leaders decide, act and create value

We integrate AI into strategic and operational decision-making: where it truly matters

No experiments without impact: we ensure all initiatives are directly linked to business outcomes

We bridge the gap between strategy, technology and execution in complex insurance environments

We empower leadership teams with frameworks, tools and clarity to make better decisions under uncertainty

WHAT SETS US APART

Where others focus on technology, we focus on decisions

K2G operates at the intersection of three critical domains

Deep understanding of insurance business models.

Integration of human judgement and AI, enabling hybrid intelligence.

Focus on decision quality, not just data quality through an end-to-end solution, covering strategy to execution.

OUR PROCESS

From decision challenge to measurable outcome

01. Define

Define the Decision Structure

We help you identify what is the critical decision that drives value.

02. Transform

Build Intelligence

We combine data, AI and expertise into actionable insights.

03. Streamline

Enable Leadership Alignment

We ensure decisions are understood, aligned and supported.

04. Deploy

Deliver Business Impact

We support execution until outcomes are visible and measurable.

USE CASES

Where we create impact in Insurance

Underwriting optimization through AI-supported decision models

Strategic portfolio and growth decisions

Claims management transformation with data-driven insights

Operational decisions frameworks for efficiency and scalability

AI-enabled pricing and risk assessment strategies

PROVEN IMPACT

Results backed by data

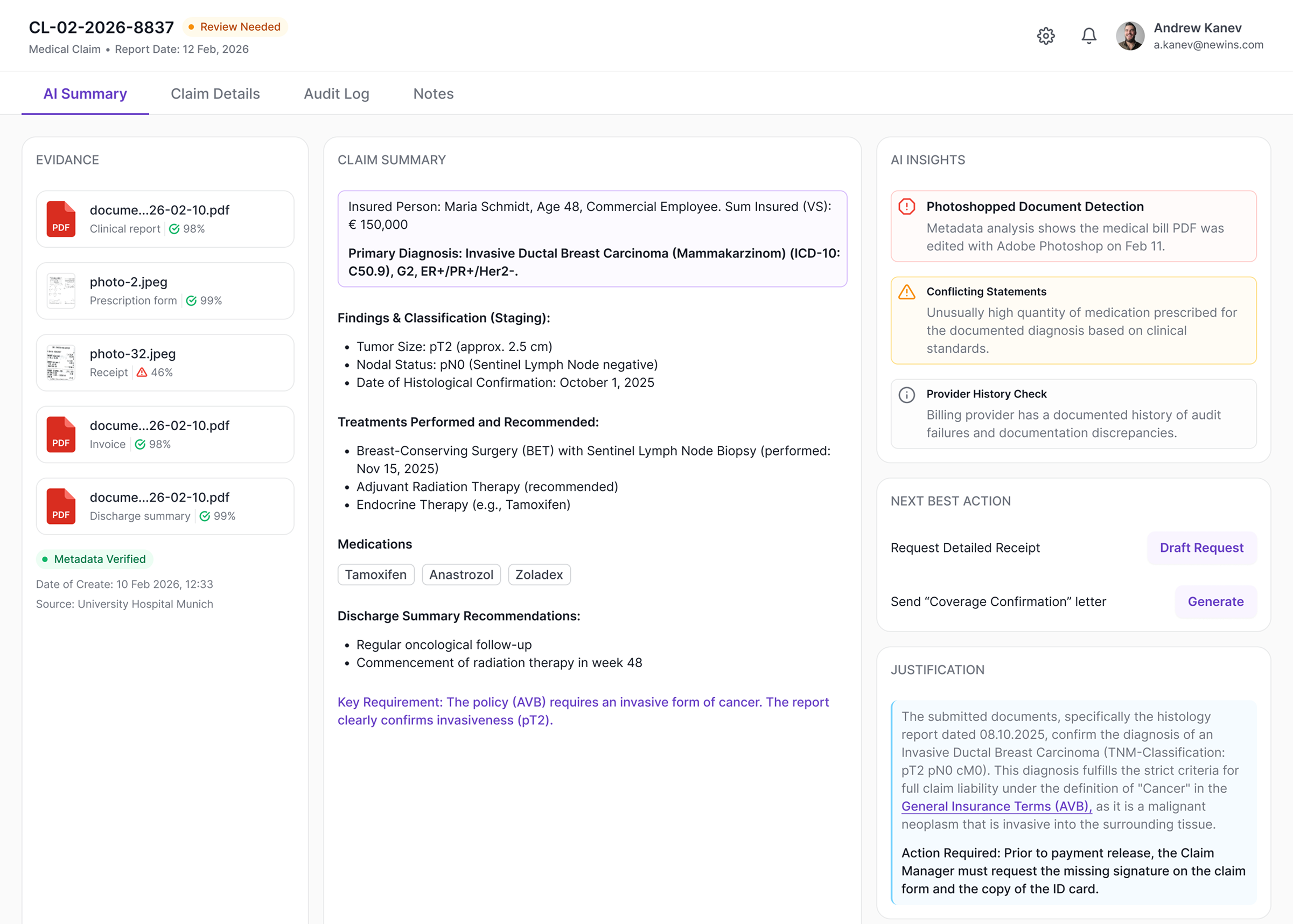

Proven results from insurers who already use K2G AI Agents to transform their pricing, risk management and portfolio growth.

Define the Decision Structure

We help you identify what is the critical decision that drives value.

Market Share

Leverage alternative data and real-time monitoring to capture new opportunities.

Time-to-Analysis

Automate repetitive actuarial and underwriting tasks to accelerate decision-making.

Pricing Accuracy

Achieve higher precision in risk-based pricing and reduce financial exposure.

TRUST & COMPLIANCE

Full Regulatory Compliance

At K2G we take security and compliance seriously. With K2G you can trust your data is in safe hands.

GDPR-compliant architecture with local processing.

ISO 27001 standards for enterprise-grade security.

DORA-ready resilience for modern insurance operations.

We don't implement AI.

We make it valuable.

K2G is a partner for insurance leaders who understand that the future is not about more data. It's about better decisions.

Ready to improve your decision-making?